By: Ted Jacoby III & Mike Brown.

America has fallen in love with protein. Supermarket shelves are weighed down with protein drinks, protein bars, protein yogurt and more.

GLP-1 drugs may have helped accelerate the protein trend, but this is bigger than Ozempic. The shift is global, it predates the drugs, and it looks like it’s here to stay. (We debated the consumer shift toward protein in our most recent episode of The Milk Check here.)

For the dairy industry, the scramble to meet that demand is splitting the whey complex in two. While WPC 80 and WPI are thriving, dry whey is increasingly an afterthought in a complex that’s reorganizing around protein.

Why Whey Wins When Protein is Hot

Whey proteins are uniquely well-suited to meet consumer demand for healthy protein. They’re functional ingredients, they’re highly bioavailable, and decades of research back their nutritional benefits.

But whey isn’t one product; it’s a spectrum. And where a product sits on that spectrum determines everything about how it’s faring in today’s market.

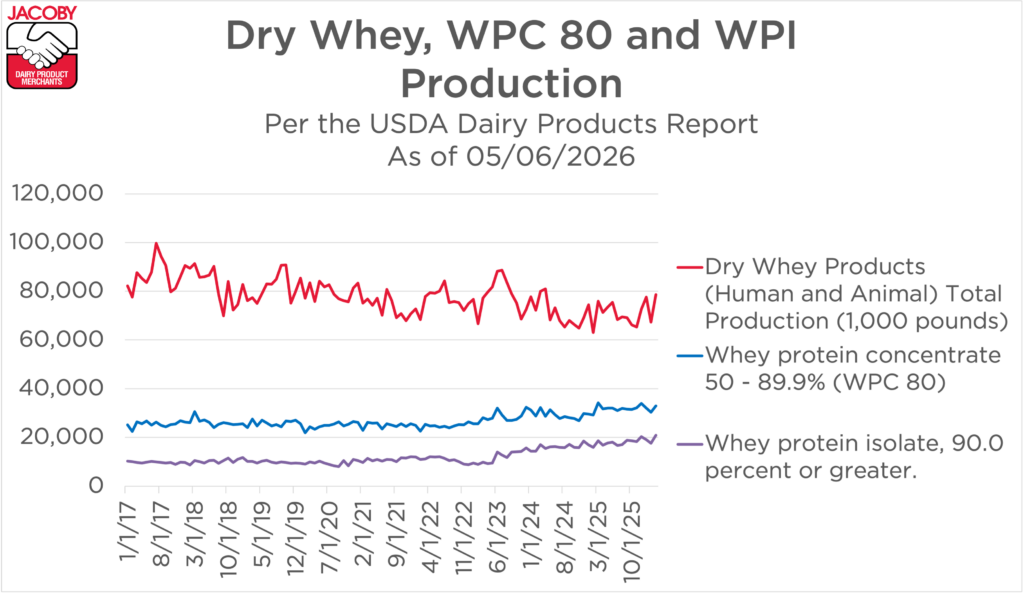

- Dry whey (~11-12% protein, mostly lactose). Used in products like baked goods, confections, animal feed, infant formula, ice cream, processed cheese. Dry whey is the commodity floor of the whey world.

- WPC 34 (~34% protein). Used in dairy snacks, soups, processed foods. More protein, more functionality, but still a workhorse ingredient.

- WPC 80 (~80% protein). Used in protein bars, shakes, sports nutrition. This is where the protein boom lives.

- WPI (90%+ protein, minimal lactose and fat). Used in premium sports nutrition, clinical nutrition, GLP-1-aligned products. The highest-value, fastest-growing tier.

The entire whey complex depends on cheese and casein production for its raw ingredient, and growing cheese output has steadily increased supply. In Q1 2026, whey production grew 4.7% faster than WPC processing capacity could absorb. The result: some of that excess whey is being dried into dry whey powder – not because demand for dry whey is strong, but simply because the whey has to go somewhere while new WPC capacity comes online.

A Market Divided

The consumer shift toward high-protein dairy has pushed processors to prioritize whey protein concentrate (WPC 80) and whey protein isolate (WPI) above almost everything else. That’s good news if you’re buying WPC 80 or WPI. It’s a more complicated story if you’re buying dry whey, nonfat dry milk, or other commodity dairy ingredients that compete for the same milk solids (a dynamic we’ve covered in depth in our look at the butterfat boom).

This is the new reality of the whey complex: protein demand is reorganizing who gets capacity and who gets supply.

What the Data Shows Right Now

Whey proteins have generally been more profitable to produce than dry whey, and the added value from protein has reached an all-time peak in the past year. Processors have pushed WPC 80 and WPI production to the limits of available capacity – and that’s a big reason prices are where they are.

The production shift is visible in the long-term numbers. Over the past 10 years, the CAGR for U.S. dry whey production is -1.2% annually, while high-protein WPC has grown at 2.7% CAGR and WPI at 6.7%.

The current snapshot tells the same story. USDA’s most recent Dairy Products Report shows WPC and WPI inventories remain well below year-ago levels, even as demand stays strong. Prices reflect that tightness. CME dry whey futures contracts range from the mid-60s to the low 70s cents per pound for the remainder of 2026, historically strong territory.

What This Means for Buyers

The protein boom is good for the dairy industry overall, but it isn’t good for everyone equally.

If you buy WPC 80 or WPI, expect prices to stay strong. Demand is outrunning capacity, new processing lines are coming but won’t arrive overnight, and the consumer trend driving all of this shows no signs of fading. The ceiling right now is how much product processors can make, not how much buyers want.

If you buy dry whey, nonfat dry milk, or other commodity ingredients, you aren’t insulated. In the short term, dry whey buyers may actually see some price relief. Processors are making less of it, but it’s also getting less attention. The longer-term risk is structural: capital and capacity are flowing away from your product category, and that trend isn’t reversing. You compete for the same milk solids and the same processing infrastructure that WPC 80 and WPI are commanding premium returns on. Investment dollars are flowing toward protein. That shapes what gets built, what gets prioritized, and ultimately what you pay, even if your product never shows up in a protein bar.

Conclusion

The whey complex has always been interconnected. What’s changed is who’s driving it. Protein is in charge now, and everyone downstream feels it.

If you’re buying or selling whey proteins, dry whey, or other dairy ingredients, contact us. We trade the full whey complex and can help you think through what this market shift means for your business.